Outlook: This week we get the ECB policy meeting and the US GDP and PCE readings It’s not hard to say which will be more important to the FX world. US GDP is forecast at 1.8% (from the wild 4.9% in Q3), although the Atlanta Fed has it a bit higher at 2.4% as of Friday, the last one for Q4 and the new one next Friday for Q1. We also get the S&P Global flash estimates of the Jan PMIs.

December PCE data (Friday) will run the table. Headline is expected to remain steady at 2.6% y/y while core is expected to fall two ticks to 3.0%. As noted, the 6-month and 3-month change in core PCE inflation is near or below the Fed 2% target and that inspires many to keep calling for the early cut.

The ECB is expected to keep rates on hold and perhaps to sound hawkish, considering chief Lagarde’s recent comments. Meanwhile, the Fed will be silent, having entered the blackout period before the Jan 30 policy meeting. That won’t stop traders from drawing conclusions from the core PCE data.

The second thoughts about the timing of the first rate cut, and the later ones, is going on everywhere, not just the US. The ECB and BoE are doing the same thing—trying to rein in over-optimism. It’s working, mostly. The ECB board members are especially firm that early rate cuts are not in the cards.

The FT reports “Gilts have endured a bruising new year as investors have a big rethink about the timing of Bank of England interest rate cuts this year. An Ice Bank of America index of UK government debt has sunk by 3.6 per cent this month — more than double its US counterpart — with much of the damage done by an unexpected acceleration of inflation.

…”While the UK’s annual inflation rate unexpectedly accelerated to 4 per cent in December, economic data has been mixed with retail sales data and wage growth this week both softer than the market had predicted.

“Still, traders in swaps markets are betting that the UK will deliver 1.1 percentage points of interest rate cuts this year, from the current level of 5.25 per cent, a 15-year high. At the start of the year traders had priced in 1.73 percentage points of cuts.”

In the US, the same “Ice Bank of America index of US Treasuries has fallen by 1.36 per cent this month, while the index of German government bonds — the benchmark for the eurozone — has fallen by 1.91 per cent.”

An exports says “gilts have been more volatile than other bond markets “mainly due to the extreme valuation anomalies we saw last year and the extremely elevated levels of inflation we saw compared to the EU and US.” Some economists predict that the UK’s underperformance compared with other major bond markets this year will be short lived.

Capital Economics thinks the UK may be the first economy to get inflation under the target as early as April, due to energy costs. “Capital Economics forecasts the 10 year gilt yield will fall from its current level of 3.93 per cent to 3.25 per cent by the end of the year.”

The CME FedWatch tool shows the percentage of those expecting a 25 bp cut at the March 20 meeting has fallen to 46.0% from 76/9% a week ago. The US rhetoric has worked.

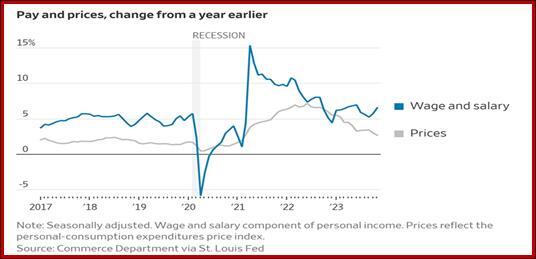

Contributing to second thoughts is on-going musings about the labor market. See the chart from the WSJ. With the participation rate falling, if not by much, some worry about the labor shortage resulting in ongoing wage increases.

Forecast: We have to wait until Thursday’s GDP and Friday’s PCE to be sure, but it looks like the US economy remains robust and the y/y inflation is not good enough for an early rate cut, even if the 6 mo/6 mo and q/q are nicely under 2%. The Fed wants a sustainable drop, and two lower entries do not cut the mustard. You’d think this would be dollar-supportive but don’t break out the bubbly just yet—the chart shows a narrow range for the euro and nobody knows what would trigger a breakout either war. We’d stay out if we could.

Tidbit: DeSantis leaving the presidential primary race means it’s going to be all-Trump, all the time from now on until the election. Rats. The leaders at Davos spoke rather a lot about it, universally condemning the lout and worried about what they would have to do to offset the damage he promises. The financial news outlets say finance leaders, especially hedge funds, are considering whether there is a replay of 2016—initial stock market rout, yields up.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

previous

previous