Trying to convince markets that pricing rate cuts is wrong requires offering guidance, something that the European Central Bank may have little interest in doing at this stage. We are, indeed, in a phase of data dependency. Expect President Lagarde to reiterate it. We don’t expect this meeting to be a turning point for eurozone rates or for the euro.

We discuss here what is our baseline expectation for the January ECB policy meeting. In short, we think President Lagarde and her colleagues are not as obsessed with the market’s dovish pricing as many believe, and that they would rather stick to pure data-dependency and avoid offering guidance rather than focusing their efforts on a rate cut pushback. In other words, do not expect a significant change in the ECB’s language this month.

The market implications – by extension – should not be material if our baseline scenario materialises. There is probably some modest room for a pick-up in rates and for the euro, as market expectations lean towards some targeted rate-cut pushback, but that should not last long. A data-dependent ECB makes markets data-dependent, meaning upcoming releases on inflation and activity in the eurozone may well have a greater market impact than ECB members’ comments.

In the chart above, we discussed what other scenarios could materialise, along with potential spillovers in FX and rates.

Rates: Near-term expectations may be dampened, but cuts are coming

Going into the January policy decision, the ECB faces a market that is discounting just shy of 140bp in policy easing over the course of the year. That situation is not much different from the one the ECB was facing in December when it felt compelled to push back against the notion of rate cuts any time soon. We do not believe the ECB’s thinking will have changed much in that regard. In fact, many of the points that were highlighted in the accounts of the December meeting were reiterated in recent remarks by ECB officials.

The ECB has, to some extent, already been able to push back against some of the very early rate cut pricing, but it was also lent a helping hand by data releases. If the ECB ever intended to really push back against early rate cut pricing, it has limited its own impact. While in December, the ECB was still shying away from spelling out rate cuts, officials are now more openly talking about the possibility of rate cuts in the summer, or under certain conditions even earlier, as Market News reported yesterday citing ECB sources. Whilst the ECB pushes back, that other shift has not gone unnoticed allowing the overall distribution of market expectations to remain lower even if tail pricings are pared.

To be sure, current pricing is excessive compared to our own ECB forecast and the ECB chief economist’s outlook for a sequence of rate cuts starting in the summer. If anything, our tactical view remains for higher market rates in the near term. But in the end, data is what it will all boil down to. What the ECB can lay out, is criteria that it wants to see before considering rate cuts. This is what officials have been doing of late with regards to the timeline of wage developments and corresponding data. It might further dampen expectations for near-term cuts, but by itself will help lift rates overall to only a moderate extent.

FX: Rangebound euro to await rate convergence

We doubt the FX market will have a big reaction to the ECB announcement unless Lagarde offers clarity on the timing of rate cuts. EUR/USD has been stubbornly rangebound recently, and above all quite detached from short-term rate dynamics.

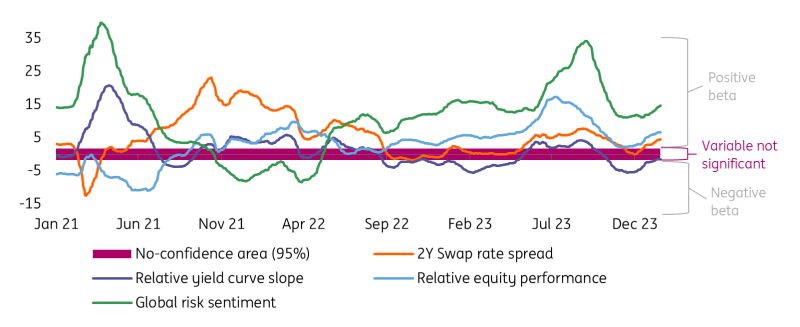

The EUR-USD 2-year swap rate differential currently sits around -115bp, the same as in October when EUR/USD dipped below 1.05, and in August, when the pair was trading around 1.09. In other words, the traditional short-term rate differential simply can’t be used on its own to determine EUR/USD short-term mis-valuation. The chart below shows the t-values of our EUR/USD short-term fair value model: the farther the t-values are from zero the more explanatory power a variable has.

T-stats on EUR/USD short-term fair value model

Source: ING, Refinitiv

Market risk sentiment and equities in general currently drive most of the EUR/USD moves. Our readers will easily find out that a price chart for EUR/USD overlaps better with a global equity index than with rate differentials. There are two main reasons for the drop in the correlation with short-term rates. First, the big equity rally in late 2023, which triggered a rotation from the dollar to procyclical European currencies. And second, the fact that the EUR/USD rate differential has remained in a very tight range for several months now, since Federal Reserve and ECB rate cut bets moved in tandem.

EUR/USD can, however, reconnect with its short-term dynamics should a convergence of EUR to dollar rates occur, for example on the back of a large repricing in ECB rate cut expectations. This is currently our baseline scenario for 2024 and the reason why we are bullish on EUR/USD.

Read the original analysis: January’s ECB cheat sheet: Giving markets the cold shoulder

previous

previous