The dovish shift in Fed forecasts in December – with three rate cuts pencilled in for 2024 – incentivised the market to push even more aggressively in pricing cuts. However, they appear to have gone too far too fast for the Fed’s liking, even though inflation is almost back to target.

Expect more pushback against a March rate cut

The Federal Reserve is widely expected to keep the Fed funds target range unchanged at 5.25-5.50% next Wednesday while continuing the process of shrinking its balance sheet via quantitative tightening – allowing $60bn of maturing Treasuries and $35bn of agency mortgage backed securities to run off its balance sheet each month.

At the December Federal Open Market Committee meeting there was undoubtedly a dovish shift. We got an acknowledgement that growth “has slowed from its strong pace in the third quarter” plus a recognition that “inflation has eased over the past year”. With policy regarded as being in restrictive territory, the updated dot plot of individual forecasts indicated the committee was coalescing around the view that it would likely end up cutting the policy rate by 75bp this year.

This was interpreted by markets as giving them the green light to push on more aggressively. Given the Fed’s perceived conservative nature the risks were skewed towards them eventually implementing even more than it was publicly suggesting. At one point seven 25bp moves were being priced by markets with the first cut coming in March.

A March interest rate cut looked too soon to us given strong growth and the tight jobs market, so the recent Fed official commentary downplaying the chances of an imminent move hasn’t come as a surprise. Markets are now pricing just a 50% chance of such a move with nothing priced for the 31 January FOMC.

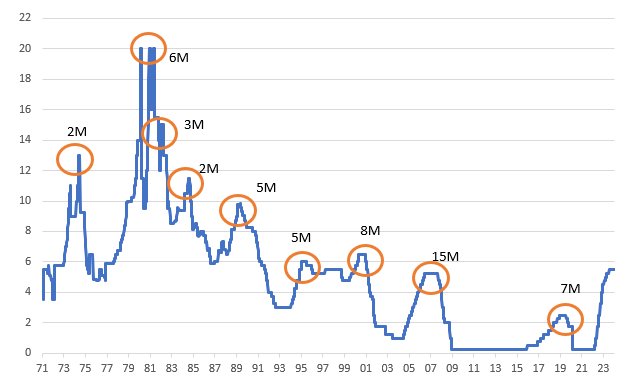

Fed funds target rate (%) and the period of time between the last rate hike and first rate cut in a cycle

Source: Macrobond, ING

But the statement will shift to neutral

In terms of the accompanying statement we do expect further changes. The December FOMC text added the word “any” to the sentence “in determining the extent of any additional policy firming that may be appropriate to return inflation to 2 percent over time”, offering a clear hint that that interest rates have peaked. The commentary ahead of the blackout period had suggested the Fed saw no imminent need for a rate cut, so we expect it to continue to push back against an early move, but continuing talk of rate hikes in the press statement is not going to look particularly credible to markets.

The Fed could choose to go back to its previous stock phraseology (used in January 2019 when it held policy steady after it had hiked rates one last time in December 2018) that “in determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realised and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective”.

And rate cuts are coming

Despite this, we believe the Fed will end up delivering substantial interest rate cuts. We continue to see some downside risks for growth in the coming quarters relative to the consensus as the legacy of tight monetary policy and credit conditions weighs on activity and Covid-era accrued household savings provide less support. Inflation pressures are subsiding with the quarter-on-quarter annualised core personal consumer expenditure deflator effectively saying ‘job done’ after two consecutive quarters of 2% prints.

The Fed’s current view is that the neutral Fed funds rate is 2.5%, signalling scope for 300bp of rate cuts just to get us to ‘neutral’ policy rates. Moreover, the ‘real’ policy rate, adjusted for inflation, will continue to rise as inflation moderates. We believe the Fed will choose to wait until May to make the first move, with ongoing subdued core inflation measures giving it the confidence to cut the policy rate down to 4% by the end of this year versus the 4.5% consensus forecast, and 3% by mid-2025. This will merely get us close to neutral territory. If the economy does enter a more troubled period and the Fed needs to move into ‘stimulative’ territory there is scope for much deeper cuts.

The Fed is knee-deep in technical adjustments, and there’s likely more to come on the QT front

One item has already been dealt with ahead of the FOMC meeting – the end of the Bank Term Funding facility. See more on that here. One of the takeaways is the notion that the Fed is comfortable with the system. That at least sends a comfort signal to the market.

In that vein, the Fed ignited an accelerated discussion on potential tapering of the its quantitative tightening (QT) agenda ahead. Currently the Fed is allowing some $95bn of bonds to roll off its balance sheet on a monthly basis. So far this has not pressured bank reserves, which are in the $3.5bn area. The Fed has been quoted as viewing this as comfortable, with the implication that they can fall, but not by too much. The 10% of GDP back-of-the-envelope target would be in the area of $3tn.

Most of the pressure from QT programme is being felt through lower reverse repo balances going back to the Fed on the overnight basis. Ongoing balances there are running at around $550bn, down by some $1.8tn since March 2023. That pace of fall is in excess of the monthly pace of QT. The residual is accounted for by a rise in the US Treasury cash balances at the Fed.

Bottom line, there are two sources of comfort here. First, room from the reverse repo balance of $550bn. That can get to zero without a material impact on bank reserves. Second, the fact that bank reserves themselves have a $500bn comfort factor between $3.5tn now to the $3tn area neutral. There is no urgency for Fed to set a plan in place, but it seems they want to get cracking on it.

It’s likely the Fed formulates a plan to slow the pace of QT over the second half of the year, as by mid-year we expect to see the reverse repo balances pretty close to zero. Maybe cut it by a third for starters. We’d then be on a glide path over the second half of 2024 where bank reserves would begin to ease lower. We’d then expect QT to have concluded by year-end. Over to the Fed to see how they deal with it.

Dollar bears require patience

We feel it is a little too early for the Fed to pump more air into the easing narrative and would probably prefer to let the data do the talking. However, the conviction is there in markets that the Fed and other major central banks will be in a position to cut later this year. This suggests that the dollar does not have to rally too far on any Fed remarks seen as less than dovish.

For the time being we see no reason to argue with seasonal factors which normally keep the dollar strong through the early months of the year. We retain a 1.08 EUR/USD target for the end of the first quarter, but expect a clearer upside path to develop through the second quarter once the first Fed cut looks imminent.

Read the original analysis: Federal Reserve to downplay chances of imminent action while holding rates steady

previous

previous