And there we have it. This week will see January in the books, and what a week it promises to be.

Not only do the Fed and the Bank of England (BoE) claim the central bank spotlight—both of which are anticipated to hold the line—plenty of macro market movers will grace the economic calendar throughout the week.

Robust US economy

According to the first estimate for US GDP for Q4, economic activity remains resilient. Real GDP rose more than expected at an annualised rate of 3.3%, tearing through the median estimate of 2.0% (down from 4.9% in Q3).

Adding to this, manufacturing and services PMIs are now both in expansionary territory (> 50.00). Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, commented: ‘Confidence has also been buoyed by hopes of lower inflation in 2024, easing the cost-of-living squeeze and facilitating the path to lower interest rates. With prices rising in January at the slowest rate since the initial pandemic lockdowns of early 2020, companies report that selling price inflation is now below the pre-pandemic average and consistent with consumer price inflation dropping below the Fed’s 2% target’.

With US consumers clearly gaining confidence (as per the University of Michigan)—a 78.8 print for the month of January, its highest point since mid-2021—and core PCE inflation slowing to 2.9% YoY, this is not an economy on the edge of a recession right now and plays into the soft-landing narrative.

Aside from the Fed’s rate decision on Wednesday at 7:00 pm GMT, another interesting watch this week will be Friday’s non-farm payrolls release at 1:30 pm GMT. The household survey’s unemployment rate (January) is expected to tick higher to 3.8% from 3.7%, and employment change is anticipated to show an increase of 173,000 new payrolls in January versus December’s 216,000 jump. A softer-than-expected reading here is likely to weigh on the buck as rate-cut forecasts could increase.

Fed expected to hold Fed funds target range unchanged

Unless you were hiding under a rock in December, the Fed’s policy meeting delivered a dovish shift with its latest economic projections. The Summary of Economic Projections (SEP) revealed that FOMC market participants project three rate cuts this year, or 75bps, up from 50bps previously forecasted. There remains a somewhat disconnect between the Fed and the market here, nevertheless, with OIS pricing around 130bps of cuts this year, and the first 25bp cut expected to emerge in the second half of Q2. For the upcoming meeting, markets are fully priced in for another no-change, leaving the Fed funds target range at 5.25%-5.50% for a fourth consecutive meeting.

A point of note for investors is whether we see Fed Chair Powell push back against a March rate cut, which, given the latest economic data, is now about a 50/50 call for the markets.

BoE anticipated to hold the bank rate at 5.25%

The Bank of England (BoE) will be live on Thursday at midday GMT. It is expected that the central bank will maintain the current Bank Rate of 5.25%. Although talks of rate cuts are not expected, the central bank could begin to strike more of a dovish tone. This may come in the form of language change in the accompanying rate statement—the central bank is likely to maintain the sentence ‘Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee’s remit’, but may remove the sentence reflecting the need to increase the Bank Rate if needed. We might also see the three dissenters (Megan Greene, Jonathan Haskel and Catherine Mann) vote to keep rates unchanged (all three voted to increase the Bank Rate at December’s policy meeting). Market pricing, according to OIS, forecasts a potential 25bp cut in June with around 100bps of cuts priced in for the year (or four rate cuts).

Inflation remains a problem for the UK. The latest report from the Office for National Statistics (ONS) revealed that headline YoY inflation rose to 4.0% in December, twice the BoE’s 2.0% inflation target and now level with France (4.1%), but still higher than Germany at 3.8%. Core CPI, which strips out food, energy, alcohol and tobacco, matched November’s release and rose by 5.1% in December YoY. Services inflation remains an issue, of course, with the latest release revealing yet another month north of 6.0% on a YoY basis for December. Consequently, the BoE are likely to exercise caution.

Overall, a language change in the Rate Statement could weigh on sterling. Likewise, a change in the MPC Bank Rate votes might also rattle the pound this week.

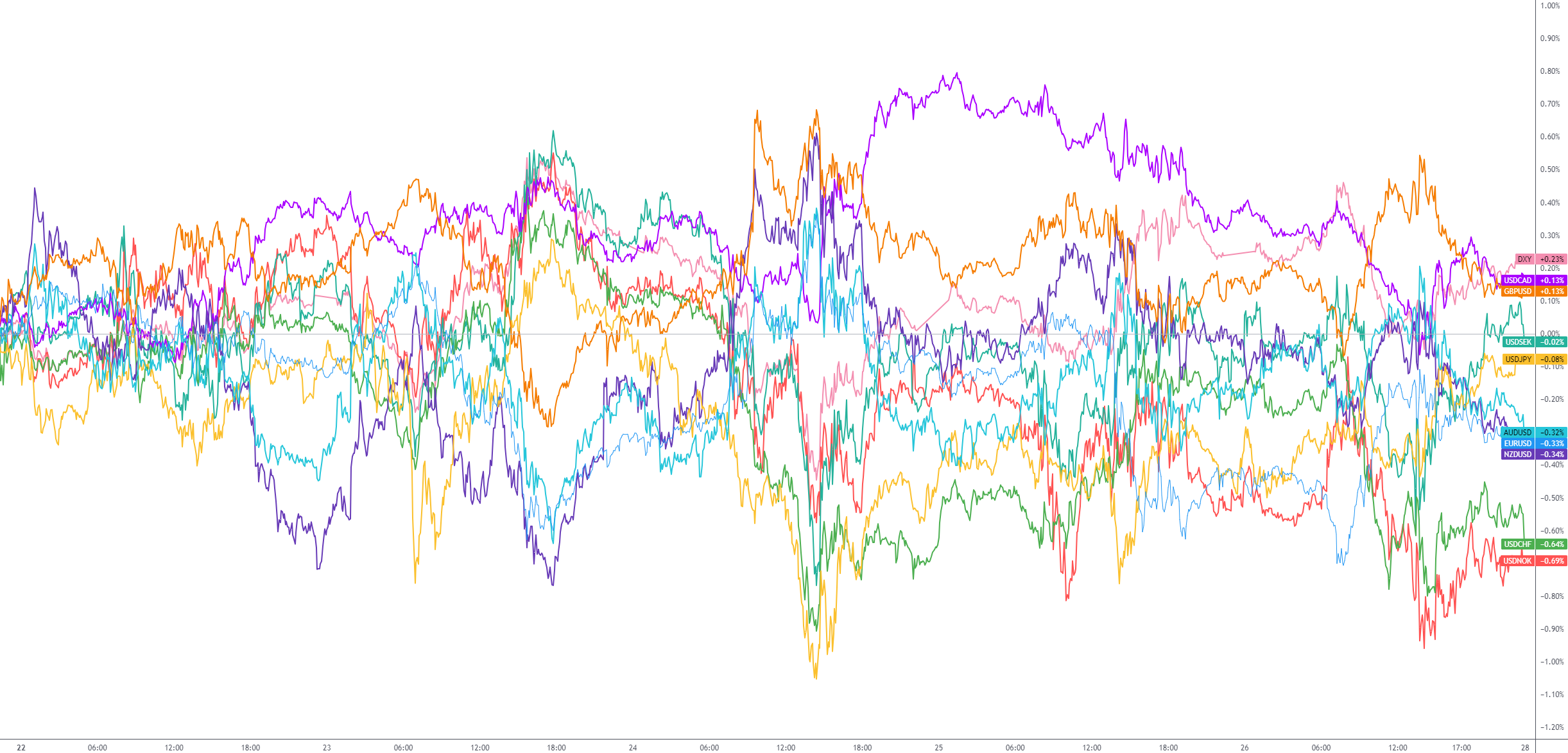

G10 FX (5-day change):

Source: TradingView

previous

previous