The Fed will hike another three-quarter point on Wednesday, at least. But looking ahead, what then?

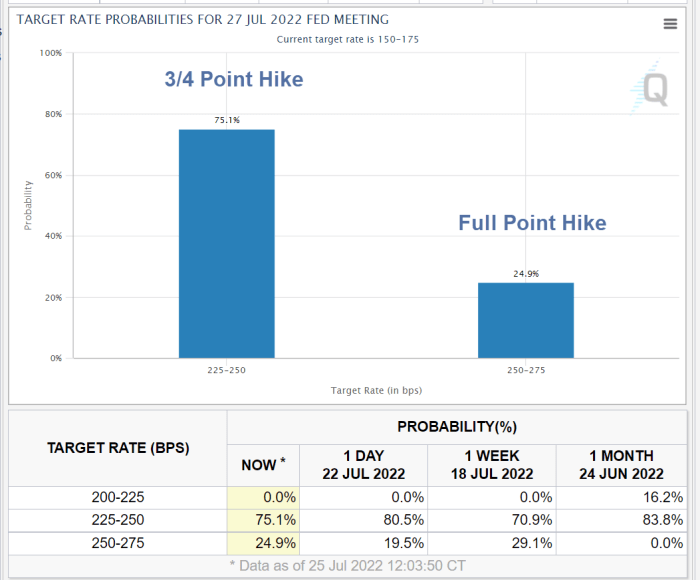

Target Rate Probabilities for Wednesday July 27 FOMC Meeting

The above chart is courtesy of CME Fedwatch.

Looking Ahead

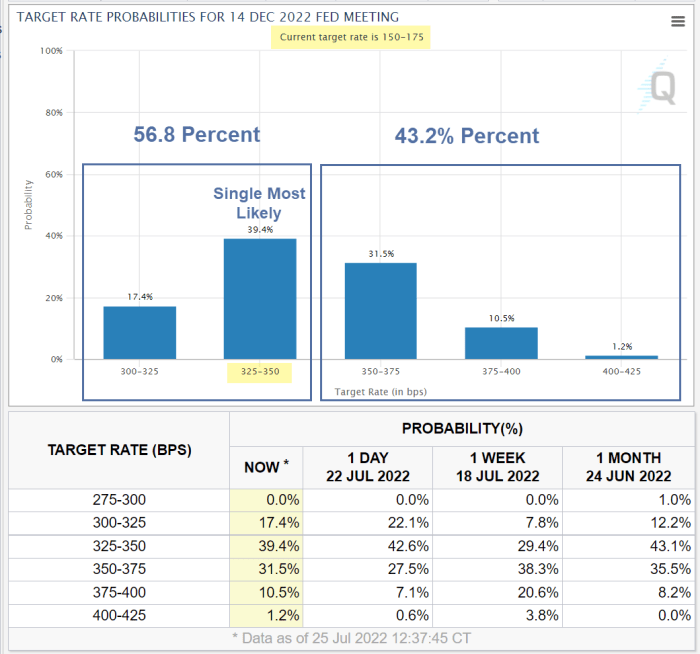

Looking Ahead to December

Target Rate Probabilities for Wednesday December 14 FOMC Meeting

Key Points

- The single most likely outcome (39.4 percent) for the FOMC meeting on Wednesday December 14 is for the Fed to target its base rate in the range 3.25-3.50 percent.

- There is a 17.4 percent chance of 3.00-3.25 percent.

- There is a significant (43.2 percent) chance of something higher than 3.25-3.50 percent.

- The second most likely outcome (31.5 percent) for the FOMC meeting on Wednesday December 14 is for the Fed to target its base rate in the range 3.50-3.75 percent.

The current rate is 1.50-1.75 percent. There are meetings on July 27, September 21, November 2, and December 14.

A 75 basis point hike in July is a given. That would takes us to 2.25-2.50 percent. To get to 3.25-3.50 percent in December would take two more 50 basis point hikes in September and December.

I am very skeptical the Fed will follow through all the way to the implied December targets.

But if inflation is still rampant (I doubt that), and the credit markets behave (doubly doubtful), the Fed will do what the odds suggest.

Powell: “We understand better how little we understand about inflation”

Let's review Powell's comments at the June 29 ECB economic forum: Powell: “We understand better how little we understand about inflation”

- Powell: “There’s a clock running here. The risk is that because of the multiplicity of shocks, you start to transition into a higher-inflation regime. Our job is literally to prevent that from happening, and we will prevent that from happening.”

- Powell: “The process is highly likely to involve some pain, but the worse pain would be in failing to address this high inflation and allowing it to become persistent.”

- Powell: “Households are in very strong financial shape. They still have a lot of excess savings from forced savings and also fiscal transfers. The same is true of businesses. The labor market is tremendously strong. Overall the US economy is well positioned to stand tighter monetary policy.”

- Powell: “Is there a risk we would go too far? Certainly there’s a risk. The bigger mistake to make, let’s put it that way, would be to fail to restore price stability.”

I strongly disagree with point three except for the labor market. The other points could not possibly be more clear, even if I do not necessary agree.

Inflation Expectations

Point #1 above is related to the idea that inflation expectations might get out of hand.

The concept is ridiculous as discussed on June 25 in The Asininity of Inflation Expectations, Once Again By Powell and the Fed.

However, Powell's position is clear: “Our job is literally to prevent that from happening, and we will prevent that from happening.”

“The bigger mistake to make, let’s put it that way, would be to fail to restore price stability.”

Expect an Overshoot

Based on Powell's comments. I expect the Fed to overshoot.

Then, unless the jobs picture or credit markets go haywire, Powell will be very reluctant to step on the gas out of fear of creating another inflation cycle.

Expect a Long But Shallow Recession With Minimal Job Losses

I expect a Expect a Long But Shallow Recession With Minimal Job Losses

But if correct, that's the good news.

The bad news is Artificial Wealth vs GDP: Why Earnings and the Stock Market Will Get Crushed

previous

previous