The big revelation – From delusions to reality

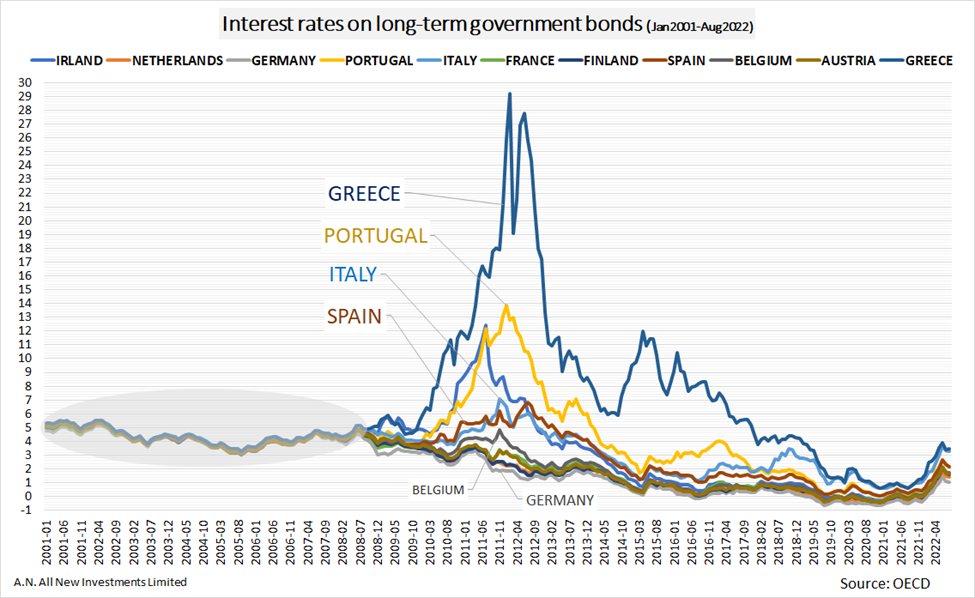

Twenty years ago, the single European currency was born to bridge nations and open new paths for European integration. The spread between the government bonds of the member states that adopted the single currency and those of Germany decreased almost to zero, even for countries like Greece, Italy, Spain, and Portugal, which will be tested by the financial crisis a few years later.

In fact, since 2001, the member countries of the euro agreed to a Stability and Growth Pact (SGP) where all were obliged to ensure that member countries pursue sound public finances and coordinate their fiscal policies. In return, all members enjoyed the cost of borrowing as Europe's powerful economies since they would borrow at roughly the same interest rates as Germany. And this was done until 2008, as seen in the diagram below.

But a few years later, with the financial crisis of 2008, everything changed. It was revealed that member states had effectively built foreign currency debt. This was true because they could not print money in Euros to avoid bankruptcy due to the high debt they had incurred. If they could do so, such a move would obviously create high inflation and currency depreciation conditions, but the member state would avoid bankruptcy.

But that didn't happen. The eurozone had changed its face and became strikingly different. As Greece, Portugal, Spain, and Italy could go bankrupt, spreads on their government bonds shot up to extremely high levels. To avoid bankruptcy and exit from the eurozone, and since they couldn't print money, they were forced to be supported by the ECB, the EU and, in some cases, the IMF in exchange for significant cuts in public financial spending. The austerity demonstrated by Europe led to the escalation of social reactions and the rise of populism and nationalism, not only in the economically weak member states.

The uncertainty lasted for quite a long time. However, things in Europe finally calmed down when ECB President Mario Draghi said the historic phrase: “he would do everything in his power to preserve the euro”. The European Central Bank has introduced Outright Monetary Transactions (OMT), a program under which the bank makes purchases on secondary markets of government bonds issued by eurozone member states. The program was accompanied by conditions of the discipline of euro member governments. Its existence was enough to reassure investors.

Everything flows – The European debt is mutualised

And while the countries since 2015 were trying to find a stabilization model, a few years later came COVID-19, which brought even more significant changes to the Eurosystem. The lockdown once again created the risk of bankruptcy in some member states, as according to the stability programs they followed, they were obliged to have small deficits or surpluses to be financed by the European Stability Mechanism.

Policymakers to avoid a new round of social and financial uncertainty in the eurozone took a remarkable decision; all member states could run a public deficit of more than 3 per cent of GDP, thus offering financing to all member states for as long as needed due to the effects of the pandemic.

With the end of the pandemic on 21 July 2022, the Governing Council of the ECB, in order to fulfil its primary mandate, which is Price Stability, approved the establishment of a Transmission Protection Instrument (TPI) in order to ensure that the direction of monetary policy is transmitted smoothly to all euro area countries.

The TPI can be activated to address unwarranted, disorderly market developments if these pose a serious threat to the smooth transmission of monetary policy across the euro area. In such a case, the Eurosystem can buy securities from individual countries in order to combat a deterioration in funding conditions that is not justified by the country's fundamentals.

This means that the central bank, unlike in the past, when the Eurosystem bought bonds of member states according to the specific weight each member has in the common currency, today in order to achieve price stability, can and does selectively buy bonds from each member state, regardless of its specific weight in the euro. In simple words, that means it mutualises the debt of the member states. This undoubtedly constitutes a considerable change in policy for Europe.

Eurobonds are here impacting euro and investment opportunities

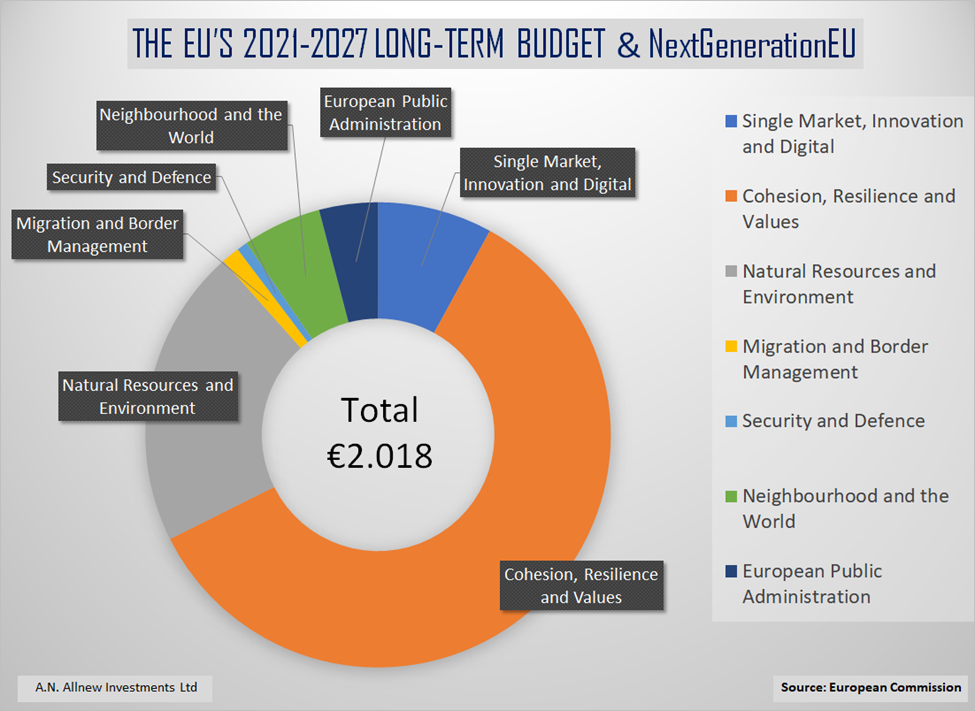

In conjunction with NextGenerationEU (NGEU), the EU's long-term budget confirms the significant changes that will take place in Europe. It is the most extensive stimulus package ever financed in Europe. The funding program was designed to stimulate recovery after COVID-19. A total of €2.018 trillion in current prices is helping to rebuild Europe by making it greener, more digital, and more resilient.

The program initiators say that “this is more than a recovery plan. It is an opportunity for Europe to emerge stronger from the pandemic, transform the member states' economies, and create opportunities and jobs for Europe, where everyone wants to live”.

It is about a two trillion-euro financial program that, in conjunction with the mutualization of the debt of the member states as described above, indicates the birth of the Eurobond, which targets specific categories of investments.

The programs are grouped into the seven spending categories of the EU budget. Each is dedicated to a specific area of investment policy.

The seven categories are:

-

Single Market, Innovation and Digital.

€149.5 billion (+ €11.5 billion from NGEU). -

Cohesion, Resilience and Values.

€426.7 billion (+ €776.5 billion from NGEU). -

Natural Resources and Environment.

€401 billion (+ €18.9 billion from NGEU) -

Migration and Border Management.

€25.7 billion. -

Security and Defence.

€14.9 billion. -

Neighbourhood and the World.

€110.6 billion. -

European Public Administration.

€82.5 billion.

Total: €2.018 trillion.

The markets view all the above changes with skepticism, also the two trillion-euro program with great interest. The euro currency in the wake of Russia's attack on Ukraine, where the EU budget was mobilized to provide emergency aid and support from the energy crisis to EU countries and Ukraine to alleviate the consequences of the war, has come under the most significant pressure from the beginning of its course.

Massive changes are taking place in Europe today. The challenges remain many and demand targeted abilities to reform the continent to strengthen it institutionally, geopolitically and economically in a new era that has already dawned.

As long as the venture succeeds, that means in the medium term, we will experience a defining period with great opportunities for European economies, companies, citizens, and investors.

previous

previous