Recent economic data paint a picture of increasing concerns about the economic outlook. In the US, high inflation and rising interest rates play a key role. In the euro area, the same factors play a role – although interest rates are still below those in the US – but skyrocketing energy prices and gas supply disruption are additional forces that should drag down growth. Easing price pressures in business surveys are a hopeful development but selling price expectations remain nevertheless exceptionally high given the weakening of order books. This could point to input price pressures that force businesses to charge higher prices to protect their margins. It is to be feared that slowing demand will make this increasingly difficult, forcing companies to cut back on investments and new hirings.

The summer break is supposed to be a period of disconnecting from the economic and geopolitical news flow. The focus shifts to relaxing, food, enjoying the weather, etc. The focus of attention flips once the holidays are over. This year is no exception, rather to the contrary. The extreme conditions in many countries during the summer months – high temperatures, drought in some countries and flooding in others, forest fires – have reminded us that the impact of climate change has become all too visible and that it entails a huge cost, not only in terms of human suffering but also for the economy.

Looking at the economic data, the picture that emerges is one of increasing concerns about the economic outlook. Although thus far it has been gradual, this development is likely to accelerate. Concerning the gradualism, high activity levels and well-filled order books still provide some resilience to the rising headwinds.

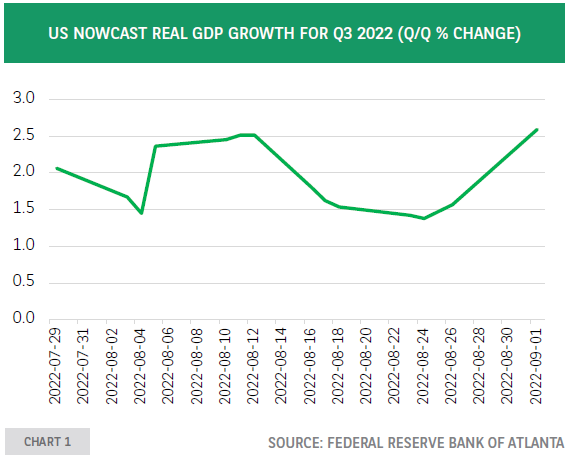

In the US, according to the nowcast of the Federal Reserve Bank of Atlanta, recent data correspond to a healthy increase of real GDP (chart 1). Job creation remains strong, and the Conference Board’s consumer confidence index has rebounded in August. However, signs of slowdown are growing. Households suffer from high inflation, giving rise to a big increase in credit card balances1. Activity in the housing sector is suffering from the rise in mortgage rates, the pace of hiring is slowing, and new vacancies are down.

The surveys of the regional Federal Reserve banks points toward a more cautious stance of companies in terms of capital expenditures. This is unsurprising considering that 81% of CEOs contacted by the Conference Board expect a brief, shallow recession in the US over the next 12 to 18 months2. Domestic demand growth will slow down further under the influence of Federal Reserve rate hikes, whereas net exports should suffer from the strong dollar and the slowdown in the rest of the world.

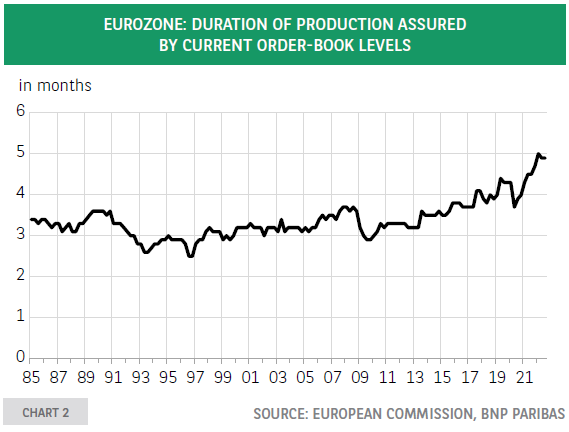

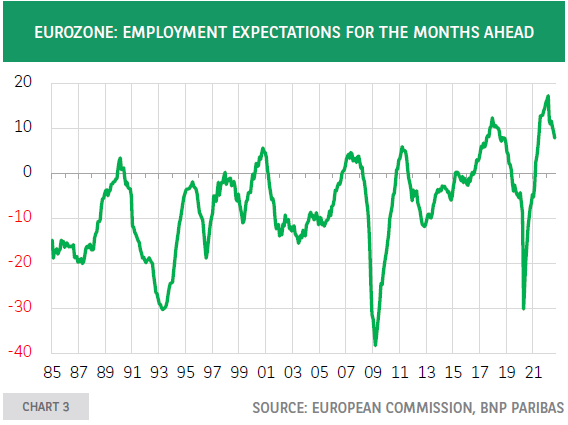

Chinese growth, after a slow rebound since late spring, has disappointed again in July and downside risks remain high. In the euro area, like in the US, a distinction should be made between the activity level and its change. In manufacturing, the duration of production that is assured by current order books remains at a record high level (chart 2) but the assessment of orders books has seen two large drops in a row. Employment expectations have also declined in recent months but remain in the upper end of the historical range (chart 3).

Based on the shocks hitting the euro area economy – high inflation, the jump in gas and electricity prices, the weakening of the euro, rising interest rates, the shutoff of Russian gas supply – business sentiment is expected to weaken further, which should weigh on the hiring intentions and investment projects of companies. As has been the case historically, this should be followed rapidly by rising unemployment expectations of households. Thus far, elevated inflation has been the key factor behind the drop in consumer confidence to historically low levels. Fears about job losses would make matters worse for consumer spending. A decline in inflation would bring some relief for households’ purchasing power, but the latest energy price shocks should delay the peak in inflation and slow down its subsequent decline. Easing price pressures in business surveys are a hopeful development.

As shown in chart 4, the assessment of order books has declined and so have the selling price expectations. However, the latter remain exceptionally high given the situation with respect to the former. This could reflect input price pressures that force businesses to charge higher prices to protect their margins. It is to be feared that slowing demand will make this increasingly difficult, forcing companies to cut back on investments and new hirings.

Download The Full Eco Flash

previous

previous