Outlook: We get a flood of data today but the important bits are the University of Michigan Jan consumer sentiment and inflation expectations, and personal income and spending and the associated PCE price index, with core expected up 0.3% m/m and 4.4% from 4.7% in November. We also get the Atlanta Fed’s first estimate of Q1 GDP, which will be fun.

A big drop in core PCE inflation would buttress the consensus viewpoint that the Fed is nearing the end of the road with only 50 bp to go, in two tranches, then a pause and then a cut in late Q3 or Q4. Never mind what any other central bank is going to do—this is dollar negative. If the core comes in closer to 4.7% again, however, all hell will break loose. Should traders cover dollar shorts?

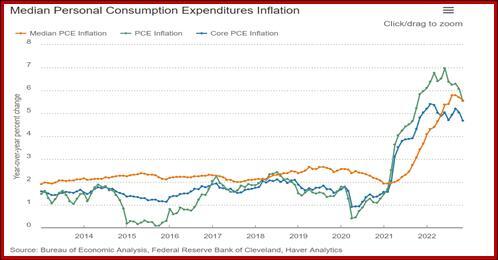

To make matters more complicated, we will get trimmed means and sticky prices from a bunch of regional Feds, too. For kicks, see the last data from the Cleveland Fed, which explains that its median PCE inflation is the rate of those things whose expenditure weight is in the 50th percentile of price changes. In other words, not some vastly expensive thing that hardly anyone buys. That means it will include eggs, which core excludes as food. “Benefits: By omitting outliers (small and large price changes) and focusing on the interior of the distribution of price changes, the median PCE inflation rate can provide a better signal of the underlying inflation trend than either the all-items PCE price index or the PCE price index excluding food and energy (also known as the core PCE price index).

Eyeballing the chart, it looks like 3-4% is about as much as we can expect in any reasonable timeframe. The probability of hitting 2% before year-end is very, very low. So, if the Fed is telling the truth, we will not be getting a cut this year as so many insist. It’s getting to the point, though, that the late-year 2023 cut is irrelevant. Far more interesting is the rising acceptance that outright recession might not be in the cards—but inflation can persist well into 2024. This is stagflation and it’s the very devil to deal with. That means we need to follow things like capital spending, capacity utilization and business sentiment to be able to predict the end of that. Maybe insider stock sales, too.

Off on the side is layoffs in tech spreading like a virus to toys and other sectors. Not that the Fed is peopled by grinches, but this is good news for the Fed. It means wage hikes will end, at least in some places, removing “wage-push” inflation worries. We fully expect to start seeing essays on how the Fed will do only 25 bp before pausing, not 50.

We have said before that the case for a strong dollar is pretty good in the long run. Assuming we get some interesting dollar short-covering now, we have to remember to call it a pushback and not a trend reversal. We don’t see full reversal on the chart yet, and of course that’s the perpetual problem with charts—like the best data, they lag.

Besides, all the really juicy big news is next week–the Fed, ECB, and BOE meetings, with payrolls as the cherry on top. Are the big players positioning on a Friday for those events? It’s complicated. If the BoE does 50 bp as expected, it will be nearing its terminal rate, but the ECB, seen as also doing 50 bp this time, will have farther to go. according to those who know how to read swaps prices. We don’t expect those forecasts to manifest in FX today. But we plan to hide under the covers on Monday.

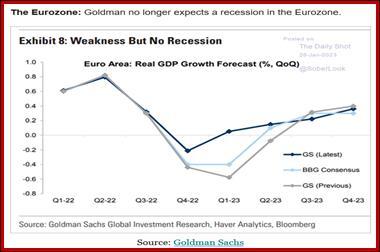

Tidbit: We would never pick a fight with Goldman Sachs, but it’s the latest to project that Europe will escape recession this year. You have to wonder what assumptions they used for the prices of gas and oil. Granted, the price of gas is now under the level of a year ago and oil is cheap, but can we really expect warm weather to keep helping? Well, maybe. For natgas in particular, Norway, the US and North Africa are filling the gap of lost Russian supplies. In fact, Russia the giant gas station is losing even that traction, the last gem in a denuded crown.

Tidbit: We are starting to see money supply stories, the latest from Reuters, now that M2 is falling like a rock, down for the 5th month and bigger amounts all the time. Year-over-year, M2 is down by over $530 billion since last March. Before then, from March 2020, M2 rose dramatically by $6.3 trillion or 40%, from pre-pandemic levels. This is QE on steroids.

We have to remember once again that money supply alone can’t drive inflation—it has to have velocity, or multiple uses in the economy. If banks just sit on the money and refuse to lend it out, you don’t get activity or inflation. See the charts from the St. Louis Fed. We do have a rise in velocity that was coupled with the rise in money supply, and almost certainly did contribute to inflation, alongside supply chain problems and other pandemic issues. The drop in money supply now, however minor ($530 million vs. $6.3 trillion) is a Good Thing and disinflationary.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

previous

previous